4 minutes

Non-703 investments can give your credit union a flexible income-management tool suited for an extended run of low interest and high liquidity.

Even if your credit union had a short-term plan for managing excess liquidity that built up in the early months of the coronavirus pandemic, it’s probably time to consider long-term strategies to bolster income as interest rates remain low.

Over the year ending in July 2020, the credit union industry’s savings balances increased 18.9%, while surplus funds rose 51.7% and assets grew 17.3%. “This is the fastest growth in credit union liquidity in over 30 years,” says Steven Rick, chief economist for CUESolutions Platinum provider CUNA Mutual Group, Madison, Wisconsin, in his September 2020 Credit Union Trends report.

Credit unions may be facing lower yield-on-assets for some time, with the Federal Reserve projecting the federal funds rate will remain at 0.1% through 2023.

Use Non-703 Instruments for Benefits and Charities

Low federal rates will hold down rates for mortgages, auto loans and credit cards, which encourages borrowers to refinance higher-interest debt, often into longer-term, low rate products such as home equity products.

If you’re looking for more flexible options to help you manage your credit union’s income in the face of these economic headwinds, consider programs that allow using investments that otherwise wouldn’t be permitted by Code of Federal Regulations, Part 703 (or Part 704 in some cases).

These non-703 investment options may not only give you greater potential for earnings than more traditional credit union investments, they can be used for two important purposes:

- Employee/executive benefits pre-funding programs can offset increasing employer costs for health insurance, retirement programs, group life and disability insurance, etc. For recruiting and retaining executive talent, non-703 investments can fund 457(b) and 457(f) plans and split-dollar life insurance arrangements, among other incentives.

- Charitable donation accounts can help you contribute more to your community at a time of great hardship for many. According to National Credit Union Administration regulations, credit unions must donate at least 51% of CDA investment returns to qualified 501(c)(3) charities at least every five years. And keep in mind that if you fulfill this and other requirements, you can retain up to 49% of the CDA’s returns as income. Notably, CDA rules can vary by state for state-chartered credit unions.

Managed Money and Insurance Products Are Key Non-703 Investments

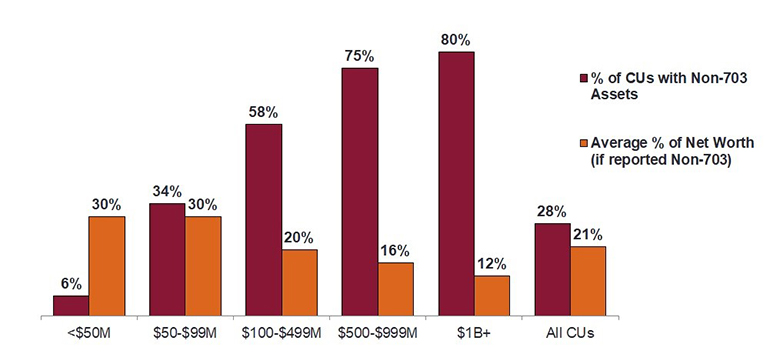

At year-end 2019, 28% of all credit unions had non-703 investments on their books, with much larger percentages among larger credit unions (see the graph below).

Below are the two main categories of non-703 investments that credit unions use:

1. Professionally managed investment portfolios

These portfolios can include directly owned securities, bonds, mutual funds and other investments that Part 703 otherwise wouldn’t allow.

2. Insurance products

Permanent life insurance policies can be used to generate conservative returns that aren’t tied directly to the stock market, but typically outperform Treasury bonds. They can be used as the basis of split-dollar life insurance agreements for supplemental executive retirement plans or as corporate-owned life insurance to fund employee benefits pre-funding programs or CDAs. Credit unions also fund these programs with other life insurance and annuity products, which feature the ability to set guaranteed floors for returns.

Put Due Diligence Measures in Writing

If you’re considering either of these two investment categories, regulatory compliance should be a priority. A general best practice is to invest no more than 25% of your credit union’s net worth in non-703 investments (with a maximum of 15% for any single non-government obligor). Anything above that level may subject you to additional NCUA scrutiny.

According to the NCUA Examiner’s Guide, examiners should look for heightened due diligence from credit union boards regarding non-703 investments, including the proper accounting procedures. It’s a good idea to have your credit union’s legal counsel and an accounting auditor review any program involving non-703 investments before you make any purchases or sign any contracts. (For more about the NCUA Examiner’s Guide and how to use the online version to manage your employee/executive benefits program, download this e-book produced by CUNA Mutual Group and CUES.)

While non-703 investments have the potential to yield better returns than other investments that credit unions typically use to manage excess liquidity, this generally means you’ll be accepting more risk. The board and leadership team should create a written policy about your credit union’s risk tolerance for these investments.

Make sure your investment policy includes regularly reviewing the product performance with providers—preferably quarterly, but at least once per year.

Once you’ve got employee/executive benefits programs or CDAs in place, they can continue to give you more choices for managing liquidity and income even when interest rates begin to rise, again, and savings rates return to normal.

Bruce Bauer is an executive benefits specialist for CUESolutions platinum provider CUNA Mutual Group, Madison, Wisconsin.