6 minutes

Use this disciplined approach as opposed to an emotional one to consider the impact of your organization’s options.

Over the last decade, the number of credit unions has declined by approximately 30%; however, mergers dwindled during the first few quarters of 2020 as the many uncertainties forced CUs to focus on internal operational effectiveness. Now that most credit unions have adjusted to a “new normal” in daily procedures, we are seeing renewed interest in strategic mergers as a viable option for long-term sustainability and relevance.

The Industry Is Actively Preparing for More Mergers

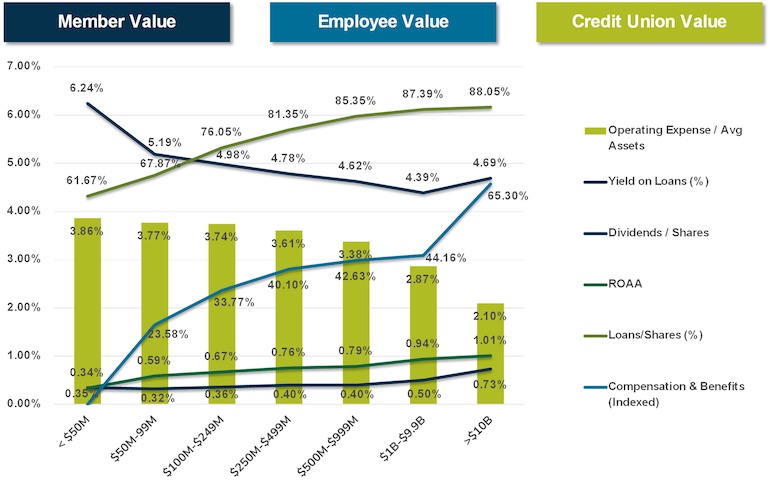

Credit unions are actively preparing for proactive and reactive mergers as the industry continues to consolidate while the macroeconomic environment remains uncertain. Now more than ever, industry leaders are focusing on achieving scale to endure reduced earnings, offering convenient service through digital and physical channels, diversifying the membership base, and improving technological infrastructure. See the graphic below, which quantitatively demonstrates how scale provides value back to members, employees and the credit union.

Such common challenges as succession planning or attracting specialized employees with in-demand skills like cybersecurity expertise may impact smaller institutions disproportionately, making mergers more attractive.

Tips to Start the Merger Process Effectively

As more credit unions prepare to explore strategic mergers, what are some of the key elements to effectively evaluate acquisition opportunities?

As with every decision a credit union evaluates, its key stakeholders are the central focus. Whether your institution is taking a proactive or a reactive approach to mergers, it will alleviate wasting time, effort, and money when its initial analysis and any resulting strategy are founded on a predetermined and well-defined value proposition for members, employees, the community, the board and the credit union. Even if your members are highly loyal and active and your credit union is satisfied with its current growth trajectory and management team, preparing for non-organic growth opportunities should be an integral part of any credit union’s strategic plan.

We recommend developing a merger assessment plan using both quantitative and qualitative assessment categories. This methodology may help establish a disciplined approach to effectively evaluate merger and acquisition opportunities.

1. Quantitative—Start with Readily Available Data

Fortunately, credit union call report data is easily accessible public information. The numbers can bring to light the initial “walk away” assessment parameters or simply identify “initial hurdles” to explore further. What would your day one probable net worth look like as a combined institution?

2. Don’t Stop There

Quantitative data shouldn’t be used merely to add your credit union and another together. The data can be used to understand the probable fair valuation (price) results, the intangible asset amortization expense, one-time costs (i.e. core system conversion) and any synergies. The results can be used to assess if the opportunity is “accretive” to the combined credit union and creates additional benefit for the members, employees and community.

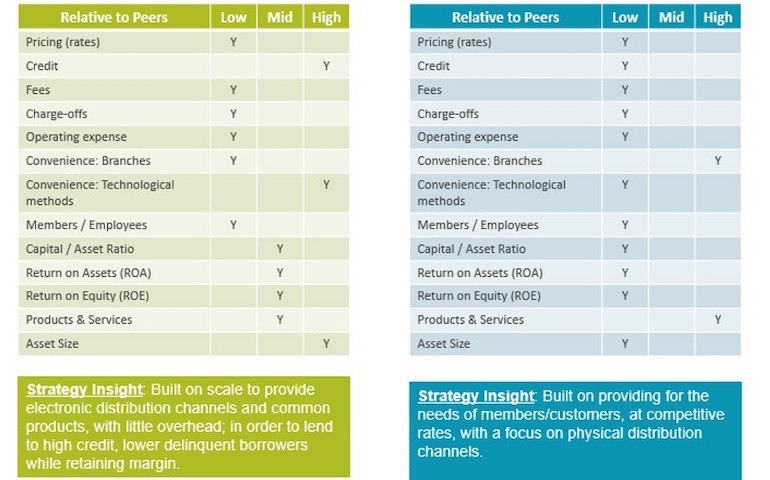

3. Consider Pricing, Focus and Strategy

Additionally, a credit union’s pricing philosophy, product and service focus, and general strategy can be evaluated and compared for fit with your credit union’s strategy. The following two examples may offer insight on how to assess a credit union’s strategy based on call reports and publicly available information.

4. The Next Step: Qualitative Assessment

If the call reports provide enough comfort to continue the process of exploring a potential partnership opportunity, it’s then best practice to perform a qualitative assessment. There is a multitude of stakeholders in a credit union merger, however, focusing on the following can provide a strong foundation.

Member Value

Evaluate how this opportunity could enhance key member benefits like convenience, more competitive pricing, expanded products and services, or enhanced service. Would this collaboration provide:

- increased access to advanced technological distribution channels in current and future expansion areas?

- practical economies of scale to benefit the entire combined membership with competitive offerings and pricing opportunities?

- an enhanced, more complete suite of products & services?

- in-person service and superior digital experiences that are adaptable and scalable to enhance member service?

Credit Union Value

Next, evaluate how the proposed opportunity could increase operational efficiency, expand access to human capital, increase revenue, offer geographic diversification, increase relevance and provide scale. Would this collaboration provide:

- an efficient, combined back office?

- access to a greater talent pool, additional career opportunities, and better compensation?

- lower member acquisition costs through greater reach and efficiency?

- increased geographic and economic diversification to better position the combined credit union for macroeconomic fluctuations and long-term viability?

- a larger organization with the ability to maintain and grow market share?

- access to a larger asset base and more capital to leverage for member benefit (technology, additional products, member service)?

Employee Value

The welfare of employees is often a key concern for credit unions as they consider merger opportunities. However, a larger organization can often provide more to employees. Consider the potential positive results like retention, increased training, and enhanced compensation and benefits. Would this collaboration result in:

- additional specialized positions as well as succession plan opportunities?

- the creation of a larger credit union that has the potential to stay more competitive on compensation and benefits?

- new roles, products and services, and expanded training opportunities for employees?

- a competitive compensation structure and expanded opportunities to incent employee engagement?

- the likelihood of being able to retain more engaged and performing employees, while also offering an opportunity for competitive retirement consideration for those at this stage of their career?

Board and Community Value

As financial cooperatives, credit union boards should also be concerned with potential impacts to the communities served. Consider how community involvement, philanthropy and long-term sustainability could be impacted. Would this collaboration:

- allow the combined organization to increase philanthropic efforts?

- motivate employees to donate time, ideas, and energy toward community causes?

- create a larger credit union with the ability to maintain long-term relevance and better serve the broader community?

5. Ensure a Combined Strategic Vision

At a minimum, the following matrix should be discussed by both credit union leaders early in the process to assess strategic fit and focus:

| Combined Vision | Cultural Compatibility |

| Areas of Synergies / Economies of Scale | Human Capital / Organizational Structure |

| Risk Tolerance | Product and Service Focus |

| Lending Focus | Membership Demographics |

| Distribution Channels | Areas of Growth / Opportunity Costs |

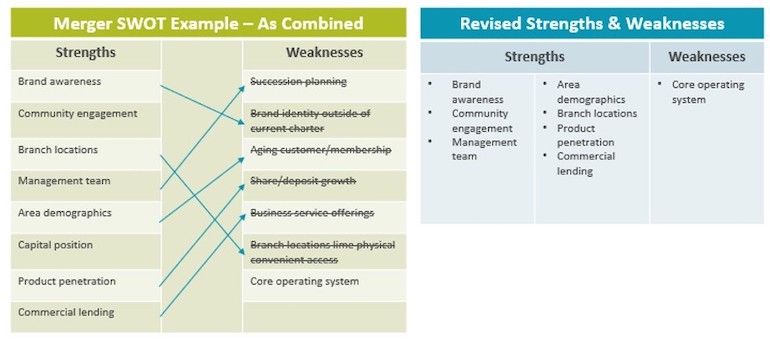

Evaluate how the combined credit union’s strengths may eliminate the individual credit unions’ weaknesses. An example of this exercise may look like the following:

6. Discuss the Transaction Structure

The following are the minimum negotiating points between two credit unions in a merger should be discussed as early as possible in the evaluation process. You must understand how important the following points are to your organization and assess how willing the other credit union is to collaborate on the following:

- Name

- Charter

- Governance

- Board Representation

- Table Officers

- Leadership

- CEO

- Executive Team

- Strategic Vision

- Organizational Chart

- Culture

- Headquarters

- Core System and Technology

By focusing on stakeholder value, analyzing these points early in the process, and asking the difficult questions right away, your credit union may effectively evaluate merger and acquisition opportunities from a disciplined approach as opposed to an emotional one.

David Ritter is managing director at CUES Supplier member ALM First, Dallas. The content in this message is provided for informational purposes and should not be relied upon as recommendations or financial planning advice. We encourage you to seek personalized advice from qualified professionals regarding all personal finance issues. While such information is believed to be reliable, no representation or warranty is made concerning the accuracy of any information presented. Statements herein that reflect projections or expectations of future financial or economic performance are forward-looking statements. Such “forward-looking” statements are based on various assumptions, which assumptions may not prove to be correct. Accordingly, there can be no assurance that such assumptions and statements will accurately predict future events or actual performance. No representation or warranty can be given that the estimates, opinions or assumptions made herein will prove to be accurate. Actual results for any period my or may not approximate such forward-looking statements. No representations or warranties whatsoever are made by ALM First Financial Advisors as to the future profitability of investments recommended by ALM First Financial Advisors.