2 minutes

Two actions to avoid in the current environment

With so many credit unions experiencing significant loan growth combined with deposit outflow in 2022, there has been little need to purchase investments. For many, simply managing adequate liquidity levels was the priority. However, as lending has started to show signs of stabilizing or even slowing down, liquidity is starting to show signs of growth. Soon, CUs could find themselves in a position to consider investing again.

Not so fast …. We are in a much different interest rate situation than we were a year ago. Sure, investment yields look particularly good right now, especially in the one- to two- year range, but we have to acknowledge the current shape of our US Treasury yield curve.

While we continue to watch the economic impact of the 2022-2023 Fed tightening cycle unfold, we have already witnessed the impact on the US Treasury Curve: inversion. This means short-term interest rates are higher than longer-term interest rates. An inverted yield curve is not a natural shape. We should be compensated more in yield the farther out we go in maturity, not less! While we don’t have the space here to really get into the ramifications of an inverted curve, just know that historically, the curve will normalize when short-term interest rates move significantly lower.

First Area to Avoid: Staying Too Short

“Why go out five years or more when you can get more yield staying in the one-year range?”

This is what the inverted curve is asking you. Well, if we believe that our inverted curve will correct with front-end yields moving significantly lower, we have to be wary of what our potential yield environment might look like when our one-year bond matures, and it is time for reinvestment.

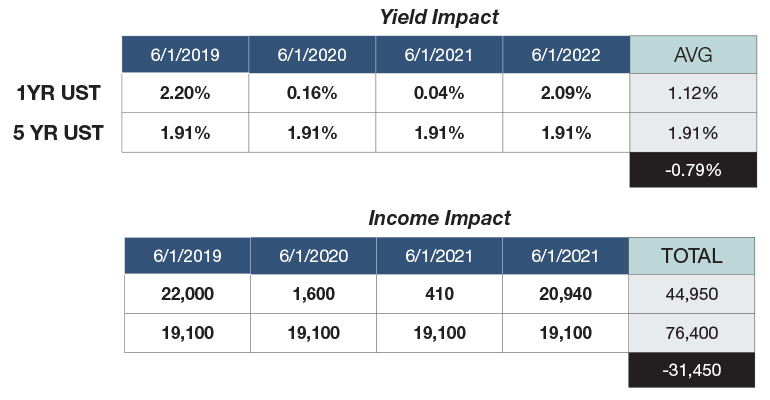

For instance, our last inversion occurred in June 2019. On June 1, 2019, we could invest in a one-year U.S. Treasury for 2.20% versus a five-year U.S. Treasury for 1.911% ... seems like an obvious decision. Fast-forward a year later and our one-year U.S. Treasury has matured. It’s time to reinvest. A year later on June 1, 2020, the yield on a one-year U.S. Treasury was 0.160%, a difference of -204 basis points.

Quick case study. Investing $1 million in a one-year U.S. Treasury and reinvesting it annually versus locking in yield with a five-year U.S. Treasury:

Second Action to Avoid: Over-Reliance on New Issue Callable Bonds

There isn’t a much more tantalizing investment than the new issue callable bond right now. Historically, the callable bond has been a favorite investment tool for the CU industry, as they offer a decent spread over agency bullet and insured CDs and are issued at par.

The problem is that the investor does not control the fate of a new issue callable bond (a.k.a. optionality). Does this really matter?

Simply put, yes! When rates start to move lower, the issuer will be incented to call your bond away so that they can re-issue at the lower prevailing rates. You get all of your money back earlier than expected, and that high coupon bond is no longer earning income in the portfolio.

The lure here is to reinvest in the new callable at the lower coupon rate. This is the start of what we call “the callable bond trap.” As yields continue to move lower, this steady process of call/reinvest can become a vicious cycle that eventually finds us at the low point of yields. As interest rate cycles go, at some point we will transition into a rising rate environment. Now, instead of the lower coupon bond getting called, it stays in the portfolio as yields march higher. In 2022, rates moved higher at a pace that made it very difficult to avoid getting stuck with low coupon callable bonds in the portfolio. These bonds are now a drag on income and unrealized losses (devaluation) for the credit union.

In closing, take heed of the curve inversion and what it could mean for the overall direction of yields. We have shared two potential investment missteps that we have observed during similar yield curves in that past.

Kevin Lynch is managing director/investments with the credit union investment strategy group of Oppenheimer & Co. Inc., a CUES Supplier member. His team provides comprehensive investment strategies and recommendations to help credit unions meet their financial objectives. With more than 35 years of investment and consulting experience, the group continues to work with credit unions nationwide, with assets ranging from $20 million to over $10 billion. Oppenheimer knows there are investment strategies available to CUs that can perform quite well in a falling rate environment, both from an income protection and a yield enhancement perspective. Interested in learning more about our strategies? Reach out to schedule your complimentary portfolio strategy call. Or contact us directly at 517.333.7760 with any questions or concerns. © Oppenheimer & Co. Inc. Transacts Business on All Principal Exchanges and Member SIPC. #5692446.1