5 minutes

Traditional methods of risk assessment may not offer a complete picture in the age of COVID-19.

For years, credit scores have been an industry-standard tool-for helping lenders determine creditworthiness. Under normal circumstances, they have provided a reliable indicator of whether a member will repay a loan on time.

But the lending environment today is anything but normal. CU Rise Analytics has been monitoring spending patterns by analyzing data from credit union clients representing more than one million members across the U.S. The results reveal that traditional methods of assessing risk may no longer offer a complete picture in an age where the coronavirus pandemic has changed everything.

What Credit Scores Can’t See

Typically, an extended period of unemployment, underemployment or other financial hardship would raise red flags. Late payments, growing debt and new lines of credit might start to appear and clue a lender into potential risk. But under the weight of the ongoing pandemic, a variety of relief efforts—which are greatly needed by many—have produced the unintended consequence of blurring the picture of risk.

Through the CARES Act, stimulus payments and enhanced unemployment benefits have helped keep many Americans afloat. Borrowers with federally backed mortgages and student loans who are directly or indirectly suffering hardship due to COVID-19 can request forbearance from a lender for up to a year. Many lenders, including credit unions, are implementing their own relief efforts as well, which include auto and personal loan deferrals and skip-a-payment programs. If a loan is current at the time relief is granted, it remains reported as current until the forbearance or deferral period is up.

These efforts have helped suppress delinquencies and defaults and ensure that a member’s credit report and credit score aren’t negatively impacted by pandemic-induced hardship. They have also obscured key insights for lenders who have an obligation to understand a member’s financial circumstances and responsibly extend credit.

Changes in Spending Behaviors

Anyone who lived through the “great toilet paper shortage of 2020” understands how significantly (and sometimes unpredictably) the pandemic impacted spending patterns.

Spending analysis by CU Rise revealed another effect of the pandemic relief efforts: Members are prioritizing repayment of their obligations differently than before. Currently, the order of priority is as follows:

- Utility bills

- Unsecured debt

- Secured debt

This is a marked departure from the past. Typically, secured debt would be a top priority when there is risk of losing collateral. With the availability of debt relief and the credit rating protection it offers, it appears that for many, repaying loans may be a lower priority—at least for now.

Despite deep pockets of financial distress, data from Experian that looked at credit scores during the first half of 2020 shows 84% of consumers stayed in the same risk tier—and 55% actually improved their credit scores. This trend combined with changes in spending behavior signals that lenders should look to indicators beyond traditional credit scores to gain a clearer and more accurate assessment of a borrower’s financial health—particularly when underwriting loans.

A New Metric for Risk Scoring

There are a multitude of factors that can be assessed in conjunction with standard credit bureau information to give a more complete assessment of risk. And the good news is your credit union already possesses this valuable information.

Utilizing a new statistical model, the CU Rise Risk Score analyzes a set of identified parameters which indicate a negative change in credit health. The CRR looks at data points such as a decline in deposits, discontinued payroll, a rise in unsecured loans, increased reliance on lines of credit, overdraft opt-in and measurable drift in deposit and withdrawal activity, combined with relevant historical markers. Each attribute is appropriately weighted and synthesized to produce a score from 0 to 100. The higher the score, the greater the risk.

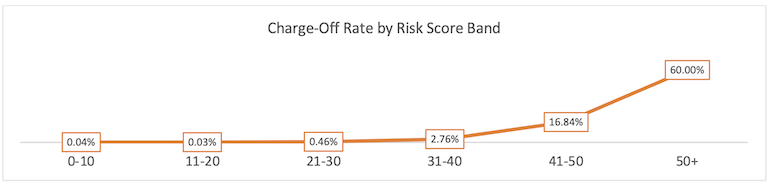

To validate the efficiency of this score, charge-off percentages were mapped to each CRR score band. A significant uptick in charge-offs happens at CRR scores of 40 and above. With a CRR score of 41-50, 16.8% of members had charge-offs. At a CRR score 50 or higher, it shoots up to 60%.

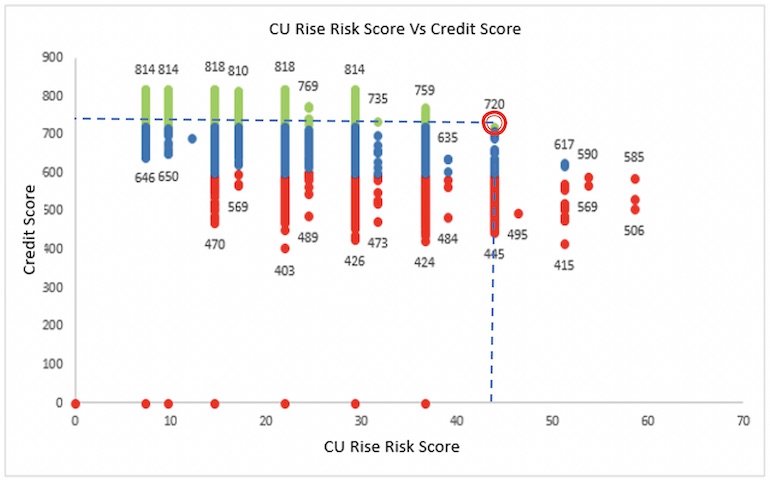

The relationship between credit scores and the CRR was also studied to examine the cross section of members who have good credit scores but high CRR scores. In a traditional lending scenario, these members might receive automatic loan approval.

The graphic above illustrates the example of a member with a credit score of 720 but a CRR score above 40. This member would ordinarily qualify for a loan based on the high credit score, but the elevated CRR score flags the borrower with the potential of high delinquency. In this case, extra caution and due diligence should be taken when extending credit.

Applications Beyond Underwriting

The CRR score has utility beyond underwriting new loans. Examples include:

- identifying current borrowers that may require closer monitoring, and triggering proactive interventions and intensive servicing that minimize financial losses;

- flagging members that should be excluded from loan marketing campaigns until their financial health improves, as indicated by a lowered CRR score; and

- incorporating CRR scores as an additional tool for loan reviews and portfolio management.

As much as everyone is ready to move beyond the pandemic, it’s becoming increasingly clear that we can expect the effects to linger. We all must adjust accordingly. The CRR score is one way for credit unions to adapt their strategies to reflect a new, ever-changing reality and how it’s changing the analysis of risk.

Suchit Shah is founder and COO of CUES Supplier member CU Rise Analytics, a leading data analytics and business intelligence CUSO headquartered in Vienna, Virginia. Learn more at www.cu-rise.com.